Per Stirpes vs. Per Capita Beneficiary Designations

While a will covers the distribution of most assets upon your death, any that require beneficiary designations, like 401(k), IRAs, annuities, or life insurance policies, are distributed according to the beneficiary designation for that account. Those designations will drive a major portion of the distribution of your financial assets. This article will explain the difference between ‘per stirpes’ and ‘per capita’ distributions so you can make an informed decision when updating your beneficiary designations.

Though beneficiary designations are an important tool to utilize, there are nuances that people must understand in order to make an informed decision. Any time a beneficiary has children, you need to be aware of how the money will flow if the beneficiary dies before the account holder. However, please keep in mind that your account documents may define these terms differently, so you need to read all instructions carefully, and feel free to contact Fausone & Grysko, PLC for assistance.

If All Beneficiaries Survive the Account Holder…

If all beneficiaries survive the account holder, then they will take their designated share, regardless of whether per stirpes or per capita is selected, and regardless of the number of children each beneficiary has.

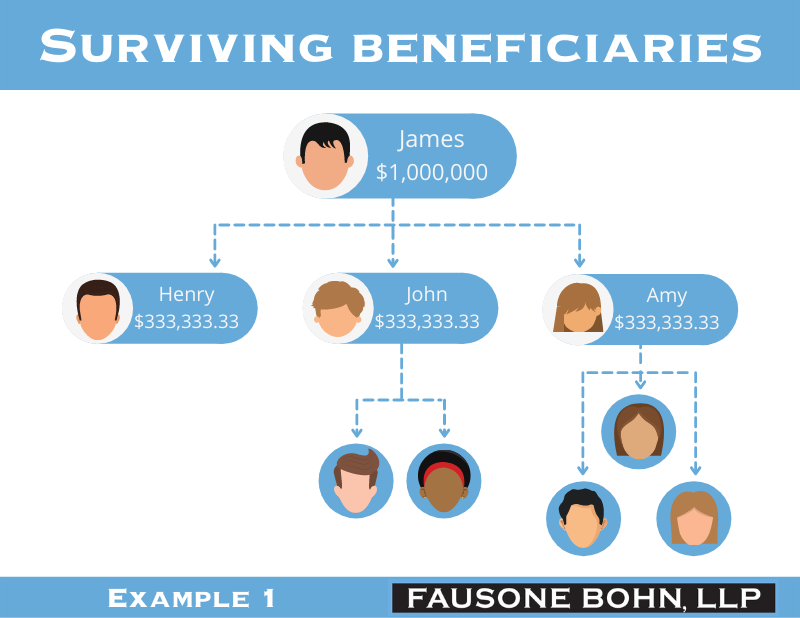

This is illustrated in Example #1, in which our fictional friend James leaves an equal 33.33% share of his $1,000,000 IRA to each of his children.

Example #1: James Doe has an IRA with $1,000,000. He has three children:

Child #1: Henry – No children

Child #2: John – 2 children

Child #3: Amy – 3 children

In this example, each child would receive about $333,333.33.

Per Stirpes Distribution

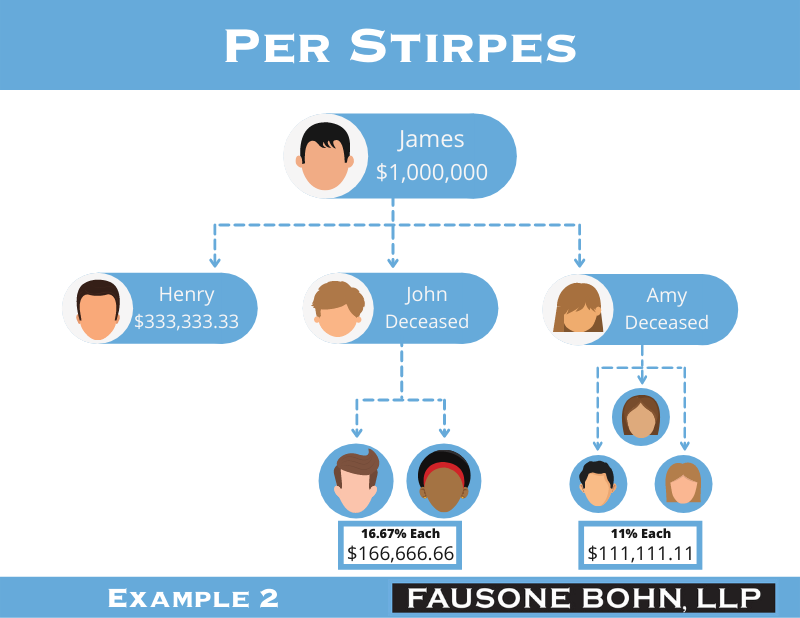

With per stirpes distribution, when a beneficiary predeceases the account holder, then any assets that would have gone to that person are then distributed to their surviving descendants instead. Per Stirpes distribution keeps assets within ‘the branch’ of the deceased child’s family, by passing that exact share on to the surviving descendants, as illustrated in Example #2.

Example #2: Same as Example #1, but assume John and Amy died before James, and James left one-third of his IRA to each child, PER STIRPES:

Henry receives 33.33%, about $333,333.33

John’s children split his share, each receiving 16.67%, about $166,666.66

Amy’s children split her share, each receiving just over 11%, or $111,111.11

Per Capita Distribution

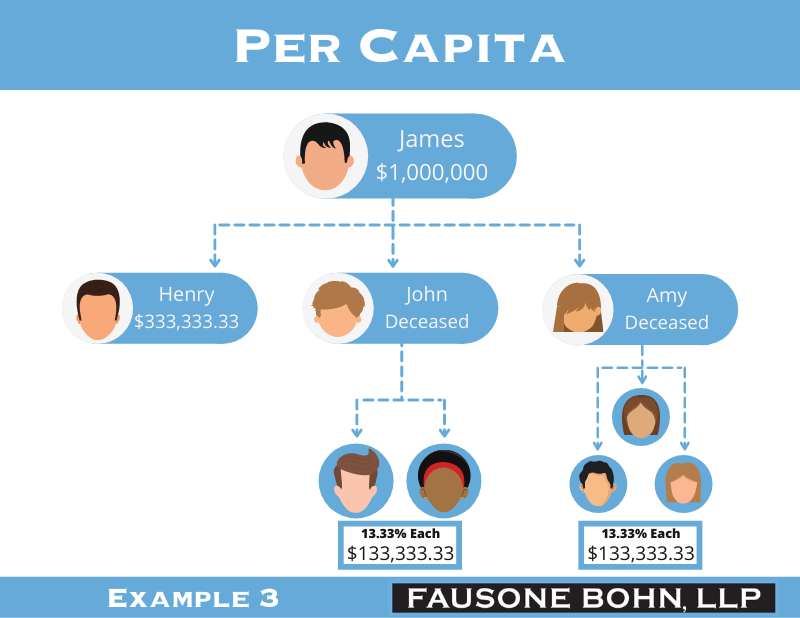

Per capita distribution also passes assets to the next generation, but it works a little differently. In this model, the shares allocated to deceased beneficiaries are combined into one pot and then divided up by the total number of beneficiaries in the next generation.

In considering per capita, it’s helpful to consider another example:

Example #3: Same as Example #2, James left one-third of his IRA to each child, PER CAPITA:

Henry receives 33.33%, about $333,333.33

John’s children each receive 13.33%, about $133,333.33

Amy’s children each receive 13.33%, about $133,333.33

Why does it work out this way? Remember, the one-third share of John’s and the one-third share of Amy’s are combined into a single share of two-thirds. That share is then divided by 5 (the number of grandchildren).

As you can see, your selection of either the per stirpes or per capita method is important for contingency planning.

Estate Planning & Probate Experts | Fausone & Grysko, PLC

There are countless scenarios that could play out when it comes to per stirpes and per capita, but too many to include in one article. That is why it is crucial to periodically revisit your estate plan. In general, it is good practice to review your estate plan every time someone passes away, someone is born, or after any other significant life change – like a marriage or divorce.

It’s critical to understand the rules of beneficiary designations because they can also come into play with your will or trust. If you want an attorney who focuses on client education, contact Attorney Brandon Grysko today at Fausone & Grysko, PLC. Brandon can be reached at (248) 380-0000 or by contacting us online.